弊社は製品に自信を持っており、面倒な製品を提供していません。

弊社は製品に自信を持っており、面倒な製品を提供していません。

返金するポリシーはありますか? 失敗した場合、どうすれば返金できますか?

はい。弊社はあなたが我々の練習問題を使用して試験に合格しないと全額返金を保証します。返金プロセスは非常に簡単です:購入日から60日以内に不合格成績書を弊社に送っていいです。弊社は成績書を確認した後で、返金を行います。お金は7日以内に支払い口座に戻ります。

CIMAPRO15-P01-X1-ENGテストエンジンはどのシステムに適用しますか?

オンラインテストエンジンは、WEBブラウザをベースとしたソフトウェアなので、Windows / Mac / Android / iOSなどをサポートできます。どんな電設備でも使用でき、自己ペースで練習できます。オンラインテストエンジンはオフラインの練習をサポートしていますが、前提条件は初めてインターネットで実行することです。

ソフトテストエンジンは、Java環境で運行するWindowsシステムに適用して、複数のコンピュータにインストールすることができます。

PDF版は、Adobe ReaderやFoxit Reader、Google Docsなどの読書ツールに読むことができます。

更新されたCIMAPRO15-P01-X1-ENG試験参考書を得ることができ、取得方法?

はい、購入後に1年間の無料アップデートを享受できます。更新があれば、私たちのシステムは更新されたCIMAPRO15-P01-X1-ENG試験参考書をあなたのメールボックスに自動的に送ります。

あなたのテストエンジンはどのように実行しますか?

あなたのPCにダウンロードしてインストールすると、CIMA CIMAPRO15-P01-X1-ENGテスト問題を練習し、'練習試験'と '仮想試験'2つの異なるオプションを使用してあなたの質問と回答を確認することができます。

仮想試験 - 時間制限付きに試験問題で自分自身をテストします。

練習試験 - 試験問題を1つ1つレビューし、正解をビューします。

割引はありますか?

我々社は顧客にいくつかの割引を提供します。 特恵には制限はありません。 弊社のサイトで定期的にチェックしてクーポンを入手することができます。

Tech4Examはどんな試験参考書を提供していますか?

テストエンジン:CIMAPRO15-P01-X1-ENG試験試験エンジンは、あなた自身のデバイスにダウンロードして運行できます。インタラクティブでシミュレートされた環境でテストを行います。

PDF(テストエンジンのコピー):内容はテストエンジンと同じで、印刷をサポートしています。

購入後、どれくらいCIMAPRO15-P01-X1-ENG試験参考書を入手できますか?

あなたは5-10分以内にCIMA CIMAPRO15-P01-X1-ENG試験参考書を付くメールを受信します。そして即時ダウンロードして勉強します。購入後にCIMAPRO15-P01-X1-ENG試験参考書を入手しないなら、すぐにメールでお問い合わせください。

あなたはCIMAPRO15-P01-X1-ENG試験参考書の更新をどのぐらいでリリースしていますか?

すべての試験参考書は常に更新されますが、固定日付には更新されません。弊社の専門チームは、試験のアップデートに十分の注意を払い、彼らは常にそれに応じてCIMAPRO15-P01-X1-ENG試験内容をアップグレードします。

CIMA P1 - Management Accounting Question Tutorial 認定 CIMAPRO15-P01-X1-ENG 試験問題:

1. A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company's planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company's normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning.

The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

Select ALL the benefits for the company that could occur following the introduction of an activity based budgeting system.

A) Under an activity based budgeting system, resource allocation is linked to the strategic plan is prepared after considering alternative strategies. This approach ensures that new activities that are required to meet the company's strategic objectives are included in the budget.

B) The approach under an activity based system is to make arbitrary cuts in order to meet overall financial targets.

C) ABB systems present costs under functional headings i.e. the emphasis is on the nature of the cost. The weakness of this approach is that it gives little indication of the link between the level of activity and the cost incurred.

D) Activity based budgeting allows the identification of value added and non-value added activities and ensures that cuts are made to non-value added activities. ABB is also useful for review of capacity utilization.

E) Under an activity based budgeting system the focus is on existing resources and operations. Adjustments are then made for changes in activity and price which results in past inefficiencies being perpetuated.

Under a traditional budgeting system, only resources that are needed to perform activities required to meet the budgeted production and sales volumes are included.

F) Activity based techniques including activity based budgeting focus on the outputs of a process rather than the input to the process. This approach provides a clear framework for understanding the link between costs and the level of activity. It allows the ranking of activities and the determination of how limited resources should be allocated across competing activities.

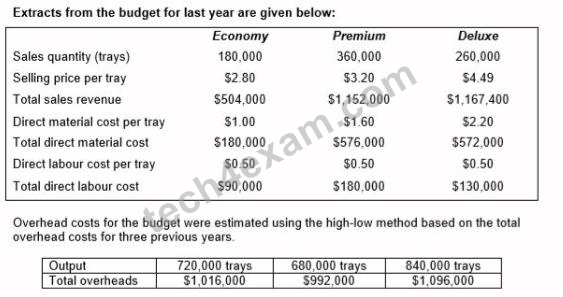

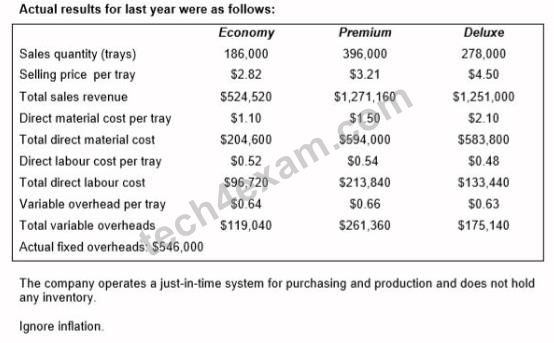

2. A company produces trays of pre-prepared meals that are sold to restaurants and food retailers. Three varieties of meals are sold: economy, premium and deluxe.

Discuss the benefits of flexible budgeting for planning and control purposes.

Select all the true statements.

A) If actual sales revenue is compared to a fixed budget it is possible to tell whether a favourable sales variance is due to an increase in units sold or an increase in sales price.

B) A fixed budget will provide meaningful control information when actual activity differs from budget and variable costs are significant.

C) The fixed budget however provides more insight into actual performance.

D) If sales volumes were well above budget, adverse variable cost variances will probably be reported, against the fixed budget, since more variable costs have to be incurred to support the higher level of activity.

E) If a flexible budget is prepared then the budget variances calculated will provide a better indication of performance since actual results will be compared against an appropriate benchmark.

F) Reporting against a fixed budget tells management nothing about the efficiency of operations.

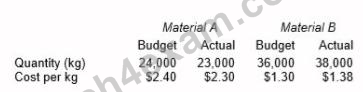

3. A company produces a product that requires two materials, Material A and Material B. Details of the material quantities and costs for August are given in the table below.

Budgeted and actual output of the product for August was 12,000 units.

The material mix variance for August is:

A) $ 1, 288 Favourable

B) $ 1, 540 Favourable

C) $ 1, 540 Adverse

D) $ 1, 540 Adverse

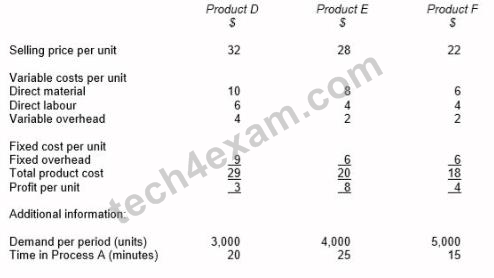

4. A company produces three products D, E and F. The statement below shows the selling price and product costs per unit for each product, based on a traditional absorption costing system.

Each of the products is produced using Process A which has a maximum capacity of 2,500 hours per period.

If a throughput accounting approach is used, the ranking of products, in order of priority, for the profit maximizing product mix will be:

A) E, D, F

B) D, E, F

C) D, F, E

D) F, D, E

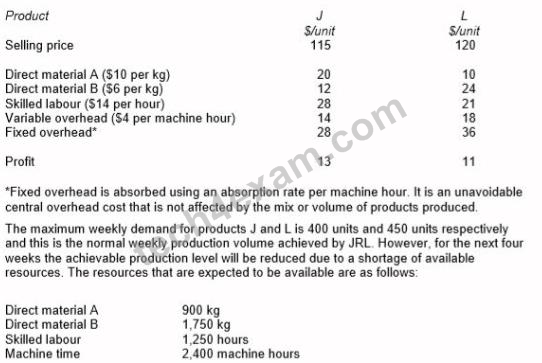

5. JRL manufactures two products from different combinations of the same resources. Unit selling prices and unit cost details for each product are as follows:

Identify, using graphical linear programming, the weekly production schedule for products J and L that will maximize the profits of JRL during the next four weeks.

A) The solution from the graph is to produce 330 units of J and 280 units of L. (A simplex solution shows the true optimum to be 332.333 units of J and 283.333 units of L.)

B) The solution from the graph is to produce 330 units of J and 290 units of L. (A simplex solution shows the true optimum to be 332.333 units of J and 293.333 units of L.)

C) The solution from the graph is to produce 317 units of J and 270 units of L. (A simplex solution shows the true optimum to be 316.666 units of J and 269.666 units of L.)

D) The solution from the graph is to produce 312 units of J and 295 units of L. (A simplex solution shows the true optimum to be 312.333 units of J and 294.999 units of L.)

E) The solution from the graph is to produce 315 units of J and 290 units of L. (A simplex solution shows the true optimum to be 316.333 units of J and 293.333 units of L.)

F) The solution from the graph is to produce 310 units of J and 280 units of L. (A simplex solution shows the true optimum to be 308.333 units of J and 283.333 units of L.)

質問と回答:

| 質問 # 1 正解: A、C、D、F | 質問 # 2 正解: D、E、F | 質問 # 3 正解: B | 質問 # 4 正解: D | 質問 # 5 正解: F |

-藤田**

-藤田**